There was some interesting reading today looking at various portfolio construction and strategy issues.

First up is that the Yale Endowment was up 1.8% in the year ending June 30th. As these sorts of pools of capital go, Yale is considered to be very sophisticated and has a long track record of using alternatives to outperform the market. For the year, that 1.8% lagged far behind the Vanguard Balanced Index Fund (VBAIX) which is a proxy for a 60/40 portfolio. Looking at a one year chart on Yahoo and sliding it so it captured June 30-June 30, VBAIX was up 7.6%. In the year ending June 30th 2022, Bloomberg says Yale was up 0.8% versus a drop of 14.97% for VBAIX.

Looking at a few other years, the year ending June 2021 Yale up 40% versus 20% for VBAIX. Year ending June 30, 2020 had Yale up 6.8% with VBAIX up 5%. In 2019 VBAIX outperformed by 221 basis points. Then you have to go back to year end June 2010 to find another year that VBAIX outperformed. A huge part of Yale's long term outperformance comes from alternatives that you and I don't have access to. I think there might be things to take away from how Yale allocates its assets when you can find those articles but I don't think it is realistic to think Yale can be mimicked.

Another Bloomberg article tried to dissect whether covered call ETFs could be suppressing the VIX Index. The concern is whether an artificially low VIX could cause an event like the Volmageddon a few years ago that wiped out a couple of short VIX ETPs. The article doesn't connect the dots on what would cause some sort of disastrous consequence for covered call funds.

I'd be less concerned about covered call funds than I would something like funds that sell puts that are anywhere near the money. There used to be a buywrite ETN that appears to be delisted but something like that could be threatened if there are any others out there. If there are any funds that replicate covered calls with derivatives of some sort then those could have trouble too. To be clear, I don't know whether any of the types of funds I just listed would have trouble but if the conversation about something breaking as happened in Volmageddon, then these would be more likely than an actual basket of stocks with calls sold against them.

Yahoo Finance wrote about 60/40 being broken but not dead. It is important to understand that the 40 year tailwind from bonds isn't repeatable. We've been saying here for countless years how risky the long end of the bond market had been as rates went lower. That thought has evolved into longer dated bonds becoming what I've been describing as sources of unreliable volatility. We've spent many years writing about ways to build the 40, or whatever percentage, without longer bonds. A different way to articulate it maybe is that just a simple, top down, active decision to avoid a ridiculously overvalued part of the capital markets saved all sorts of misery over the last 22 months or so. Of course many investors/advisors did not act preemptively but that is the nature of markets.

I sifted through a couple of the comments on the Yahoo article and there was one that caught my eye. It said that 60/40, the actual numbers, is an artificial construct, it's just made up. I don't know if that person is right but he's not completely wrong. We've built plenty of theoretical portfolios using funds that should be negatively correlated to equities that backtest favorably against 60/40 with equity allocations greater than 60%. The negatively correlated funds provide greater offset to equity market declines than bonds do. This was on full display in 2022. Also, the idea of barbelling a portfolio where a lot of risk/volatility is concentrated in a smaller portion of the portfolio can be done effectively but requires a lot more time I believe, than a "normal" portfolio.

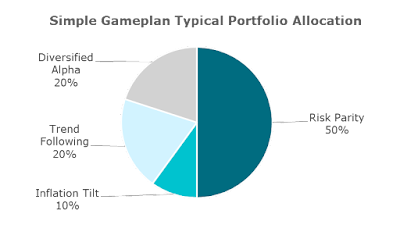

Speaking of alternatively weighted portfolios, Bob Elliott who runs the Unlimited HFND Multi-Strategy Return Tracker (HFND) weighed in with a portfolio he called Simplified Investment Game Plan.

Bob gave ideas on what funds to use to build this allocation which included the RPAR Risk Parity Fund (RPAR). I think including RPAR would sell this idea very short. I instead used the AQR Multi-Asset Fund (AQRIX) which we looked at the other day and which Rod Gordillo noted would be a better proxy for risk parity. AQRIX also goes back much further for a more useful study.

Bob favored metals for inflation and not TIPS, I used GLTR for having more diversification than a gold fund. ASFYX is a client and personal holding. Bob's explanation for diversified alpha didn't read very clearly to me. I chose two private equity firm stocks because they both seek alpha. Both KKR and APO go up more than the broad market in up trends and go down more when the broad market is dropping. The result versus just holding VBAIX.

Bob's portfolio had very rough years in 2015 and 2018 and it did very well in 2017, 2019, 2021 and of course 2022. The portfolio is intriguing of course, Elliott is a smart guy. There's no way I'm ever putting 50% of a portfolio into a single risk parity proxy. I realize I am conservative on this front but where a fund strategy is complicated, that opens the door for something to go seriously wrong occasionally. That's not a prediction, just a risk I would want to avoid. Putting 10% into precious metals is more than I ever did but I concede it is not unreasonable. We've banged the drum countless times on huge allocations into trend/managed futures. If you want to go as heavy as what Bob suggests, I would consider using several approaches. ASFYX allocates a small portion of the fund to a faster signal than the typical 10 month trend, there's a popular ETF that uses more of a replication approach sampling many managers and plenty that are plainer vanilla managed futures.

One use for Bob's portfolio that could make sense is a small account that isn't part of the larger portfolio. Someone might have their serious money in a rollover from their 401k and have a small amount in a Roth for example.

The information, analysis and opinions expressed herein reflect our judgment and opinions as of the date of writing and are subject to change at any time without notice. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

No comments:

Post a Comment