This is going to be fun thanks to a research paper by Long Tail Alpha that looks at several permutations of risk parity by reducing or replacing bonds with trend following/managed futures.

Risk parity equal weights assets by their risk (more like their volatility). Where stocks are far more volatile than bonds (usually), a risk parity program would have to own far more in bonds to equal out the volatility between the two assets. It takes so much more exposure to bonds that it needs to use leverage to get the weighting right. The paper tested several variations of risk parity and using just stocks and bonds, the weightings they used were 78% in stocks and 333% in bonds to give some idea of the leverage. The backtest with stocks, bonds and commodities weighed out at 59%, 282% and 41% respectively. The leverage is usually obtained by using treasury futures.

There are a few funds that offer one version or another of risk parity; Fidelity Risk Parity Fund (FAPYX) which started trading in 2022, the indexed Risk Parity ETF (RPAR) which started trading in 2020, the Ultra Risk Parity ETF (UPAR) which is a levered up version of RPAR, Wealthfront Risk Parity (WFRPX) and the AQR Multi-Asset Fund (AQRIX) which used to be AQR Risk Parity but does do things with leverage that resembles risk parity. Actually quite a few AQR funds do this.

One point made in the paper was that running a risk parity program requires regularly (constantly?) reassessing the risk/volatility of the assets held and reweighting accordingly. This makes sense. Look at the 78/333 blend. It seems like there'd be a lot of leeway to make changes if stocks fell 20% over the next two weeks. In that sort of instance it might make a lot of sense to ratchet up the equity exposure either by buying more stocks, selling down the fixed income or both.

"Risk parity portfolios are particularly vulnerable when their active weighting algorithms fail to

predict shifts in asset correlations." If the paper is correct about the need to do this, it undercuts the premise for indexing risk parity which is what RPAR and UPAR do. As index funds, presumably there is no sort of algo assessing correlations or anything else. RPAR has underwhelmed just about every time we have looked at it.

The authors noted that risk parity did very well for a long time but that "bond based risk-parity failed miserably in 2022." In fund form, it started doing badly long before 2022 which is corroborated by AQR's change to AQRIX in 2019. It had been struggling for a while at that point and so they changed it.

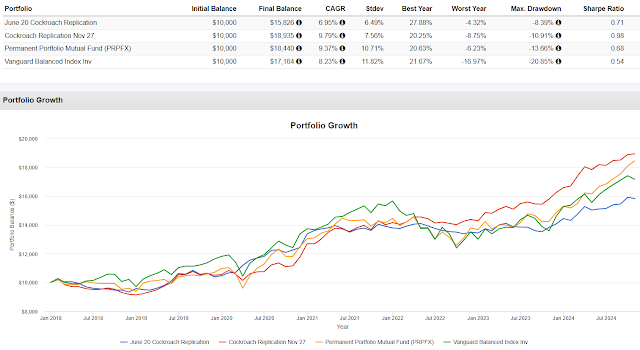

The table/chart goes back to FAPYX' inception. In the same period Vanguard Balanced Index Fund (VBAIX) which is a proxy for a 60/40 portfolio compounded at 10.89% with a standard deviation of 12.43%. AQRIX has some risk parity attributes but maybe it doesn't really belong? Either way FAPYX, RPAR and WFRPX are all tough sells. This year they are doing a little better price-wise with indexed RPAR bringing up the rear with a 5% gain through August.

Just because the investment case for the funds is weak doesn't mean we can't learn from the risk parity paper. Here are some stats adding trend to stocks and bonds in a risk parity program weighted at 67% equities, 268% bonds and 63% in trend versus the 78/333 blend for stocks/bonds we mentioned above.

Stocks/bonds/trend also had a much lower kurtosis. Kurtosis is a very fancy word where the higher the number, the greater the risk of an outlier result like 2022. A lower number is a mathematical representation of smoothing out the ride via fewer/smaller outlier results. They also compared stocks combined with bonds to stocks combined with just trend (no bonds) and stocks/bonds did much better which is surprising. That is explained by the terrific run in bonds for most of the period studied. I have been contending for a couple of years, all that was good about bonds with duration is now gone.

Then the paper looked at what it called optimized trend which is a combination of trend (managed futures) and carry. We've spent some time trying to figure out carry as ReturnStacked implements it and the paper gives what might be a more useful idea. Trend will go long markets like commodities and currencies and so on that are in favorable trends and sell short markets in unfavorable trends. Weaving carry in to optimize trend limits the strategy to going long markets in favorable trends and with a favorable roll yield aka positive carry aka backwardation. To short a market in an unfavorable trend that market would also have to be in contango, have a negative carry. That gave improved results as shown here.

Surprisingly though, the kurtosis was inferior to stocks/bonds/plain vanilla trend. The weightings for this model were 64%, 251% and 54% to optimized trend. Finally they work commodities in and the result appears to be better leaving commodities out.

Note that the kurtosis of this blend is a a fair bit higher with commodities included. And the weightings to this last one were 51%, 225%. 35% to commodities and 46% to optimized trend.

I am not aware of a managed futures fund that adds in carry in the manner discussed above. I spent some time looking but didn't make a day of it. If you know of one, please leave a comment.

The manner in which leverage was used in the paper is not accessible to retail sized investors in brokerage accounts which is fine with me. Many terrible market episodes have been caused by misusing leverage and while I am sure risk parity and the like is "different" (I am being sarcastic and snarky)....there can be a use for some leverage in a diversified portfolio like a sub 10% portfolio weighting in a fund that uses leverage. Such a fund is unlikely to end in financial catastrophe even if the fund in question blows up. That is a far cry from 333% in bonds.

Where true risk parity is out (for me anyway) and I'm not seeing with the funds, the question is whether some attributes of risk parity can work into a diversified portfolio to make it more robust? Again, the leverage used in the paper isn't accessible so I built the following to replicate RPAR. I'm not using RPAR yet because this replication allows us to go back much further than how long RPAR has been trading. The math is only off by a shade using leverage via UST and a little bit of SSO, remember RPAR is leveraged.

Taking the idea from the paper of swapping in managed futures or reducing it, I built the following.

Portfolio 2 splits the duration sleeve of RPAR with half in managed futures and half in catastrophe bonds which provide income without really taking duration risk. Portfolio 3 puts the entire duration sleeve into managed futures. Both Portfolios 2 and 3 are reduced proportionally to take leverage out.

Splitting the duration into catastrophe and trend had slightly better growth, a considerably lower standard deviation and much better Sharpe Ratio. This is probably attributable to trend having some weak years in the 2010's. The CAGR and volatility strikes me as something you might shoot for with a strategy like the Cockroach Portfolio that we've looked at many times or maybe what the Cambria Trinity ETF (TRTY) is trying to do. Both 2 and 3 were up in 2022 while the RPAR replication was down 11%.

I find this to be interesting but anyone needing normal stock market growth in order for their retirement plan to work, probably isn't going to get it from any of these portfolios.

The next table adds the actual RPAR in as the benchmark which shortens the time frame and the output is puzzling. In the replication of Portfolio 1, I tried to avoid any sort of qualitative improvement to get a better result.

The Replication is based on this from RPAR.

In 2020, RPAR did much better than the replication, did a little worse in 2021, 2023 and 2024 YTD and in 2022 RPAR lagged the replication by 11%. If you see an error on my part please leave a comment.

I've been studying risk parity for a long time. The idea is very intriguing, volatility weighting different asset classes even though the parity part of trying to equal weight the volatility is not something I believe in doing. A portfolio that equal weights assets' volatility is not going to have a normalish weighting to equities which I think is important for most investors. Normalish is a wide range, 40-70% maybe, well 40% might be a little light but you get the idea.

The volatility and correlation characteristics of the alternatives we talk about regularly here can help solve the issue of equity volatility management. I'm sure it's obvious that is where I am coming from, I write about it almost every day. One concept from way back that we talk about here is taking bits of process from various sources to build your own process. The above probably captures the little bit that risk parity contributes to my process. Portfolios I manage don't really look anything like risk parity but there is influence.

And since I mentioned TRTY above, here that fund is with the same Portfolio 2 both compared to VBAIX.

The information, analysis and opinions expressed herein reflect our judgment and opinions as of the date of writing and are subject to change at any time without notice. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.