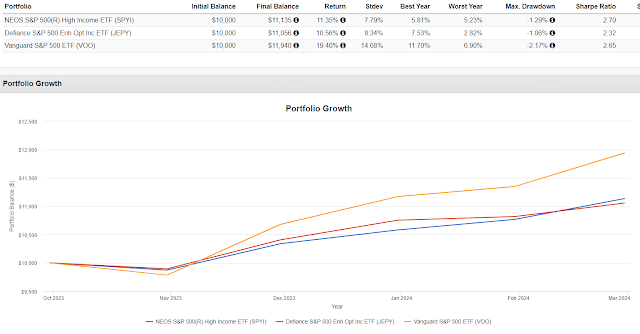

I stumbled into some content about model ETF portfolios including one interesting portfolio that was comprised of ETFs that I'd mostly never heard of. It was impressive that the portfolio was not just a collection of the largest Vanguard, iShares or Schwab ETFs. I'm not going to try to dissect the portfolio for a couple of reasons. There's no need to create the impression of bagging on the portfolio, they are trying something innovative. Also the track records of the funds is very short, and it is tactical enough that it could have a different look every couple of weeks so I'd have no way of know how it positioned previously.

With something like this, once you dig in and understand the process, you probably need to be all in an not second guess it. From there it will either work as hoped for or not. Part of the analysis needs to be what sort of tracking error might there be and why.

One of the funds in the model is the Goose Hollow Tactical Allocation ETF (GHTA). It owns equity and fixed income ETFs and has wide latitude to vary its exposures to each. Equities can range from 10%-80% and fixed income can range from 20%-90% all with the objective to "provide total return."

That description tells me that there could be meaningful deviation from whatever it benchmarks to. I may have missed but I did not see any mention of what it benchmarks to but a mix and stocks of bonds sound sort of like Vanguard Balanced Index (VBAIX) which is a proxy for a 60/40 portfolio. If GHTA's tactical process can add value around a 60/40 portfolio, that would be interesting and if you want it to add value versus something that is plain vanilla, it would have to have tracking error.

The above goes back to GHTA's inception. Right out of the starting block for GHTA, VBAIX fell off a small cliff and GHTA managed to avoid that decline. In those first three months or so, GHTA outperformed by about 8.5% which accounts for about half of it's total outperformance since inception.

For the last year, GHTA is only up about half as much as VBAIX.

It missed on some of VBAIX' rally in late May last year into June. It looks like it tracked closely for the last six months of 2023, then turned down to start 2024 and then traded flattish since mid-January like maybe it lightened up on equities? Yahoo Finance has GHTA down 0.7% this year versus a gain of 4.7% for VBAIX.

Tracking error is not necessarily a negative. Again, if you are trying to add value beyond a benchmark type of holding, you have to have tracking error. It is important then to understand what an adverse tracking error might look like and what might cause it. With GHTA, lightening up on equities at the wrong time seems like one potential cause for the fund to lag or maybe getting something wrong with fixed income duration. You can draw your own conclusion about GHTA but more generically a fund like this probably is more of a "explore" position in a core and explore type of portfolio. In 2022, an 80/20 VBAIX/GHTA blend outperformed 100% VBAIX by 378 basis points while it lagged 100% VBAIX by 70 basis points in 2023.

Circling back to model ETF portfolio mentioned at the top of this post, the asset allocation was as follows.

- US Equity 56%

- Trend Following/Tactical 38%

- Emerging Market Equity 5%

- Cash 1%

I don't know often that changes but that there is not a permanent allocation to fixed income is of course intriguing to me. The constituents I chose to mimic the above asset allocation are all very generic other than maybe EBSIX which is a pretty good managed futures fund that is not in my ownership universe.

This asset allocation looked pretty much exactly like VBAIX right up until VBAIX broke in 2022 when it declined by 18 basis point versus 16.87% for VBAIX. In the other 11 years (full and partial) it outperformed VBAIX in 6 years and lagged in 5. Anyone paying for this, in normal years it is a flip of the coin whether you'd outperform or not but either way, not much tracking error until you needed it.

That is pretty much what I try to do. Stay somewhat close and then hopefully a lot of tracking error for going down less in years like 2022. With an adequate savings rate, riding something like VBAIX up and down for every basis point will get the job done over the long term provided panic selling can be avoided. Successfully going down less in yeas like 2022 reduces the odds of panic selling which hopefully leads to a better long term result.

The appearance of not adding much value most of the time requires patience on the part of the investor. Markets go up most of the time, investors don't need protection against everything going right.

The information, analysis and opinions expressed herein reflect our judgment and opinions as of the date of writing and are subject to change at any time without notice. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.