Yahoo had an interview with Ed Slott who is a preeminent expert on Roth conversions, or at least a very well know proponent of them. This has been his thing for a long time. Part of the equation is that he is convinced that tax rates have to go up to pay for out debt and so converting to a Roth now before tax rates do go up will result in people ending up with more after tax dollars versus just going the RMD route at what is now 73 on its way to 75. I'm paraphrasing Slott.

I haven't seen too many scenarios where Roth conversions were optimal as most people don't earn more after they retire. Do the math on your particulars like what your various sources of earned income will likely be, how much your RMDs will likely be and so on.

One no brainer scenario for me for Roth conversions is one we talk about frequently where someone's hand is forced into retirement either from downsizing or health reasons or even just retiring early with no earned income. Someone in their 50's or 60's living on (qualified) dividends and long term capital gains could convert some of their dollars tax free pointing toward the standard deduction and a few more dollars at a very low effective tax rate. At $80,000 of earned income solely from a Roth conversion, Nerd Wallet has the taxable income at $52,300 with Federal tax owed at $5836. If anyone is in this situation and can pull this off, big if, then yes, it makes a lot of sense. Imagine 10-15 years of this before taking Social Security, how much of your traditional IRA would that clear out? Work with your accountant though.

With more normal scenarios, really crunch the numbers with your accountant.

Among the comments which mostly accused Slott of pedaling fear in order to sell a book was this interesting comment.

Always read the comments. This point is more interesting than the conversion idea. I won't get into this person's qualitative judgment about how much someone else needs but how much do you think you need? If you are 50 or 55 or 60, are you able to assess how likely you are to end up with what you think you need? $500,000 is fine sum to accumulate but someone who thinks they need $1.3 million but ends up with $500,000 is going to have to make some very difficult decisions and concessions.

Some goal, your number, is fine to shoot for but whatever you end up with is your reality. $1.3 million as a goal means nothing to the person who ends up with $500,000. $500,000 becomes the reality they have to adapt to.

If you have a goal, what is it based on? I have no goal, no number in the normal context. We live a $4500/mo lifestyle in terms of fixed expenses. Non monthly expenses like property tax and property/car insurance has gone up lately, maybe this year it's about $13,000. Then maybe a few thousand a year for unbudgetable one-offs like vehicle repair and veterinary bills. For us, maybe that's $6600/mo or rounded up to $80,000/yr. We do fun things, but that is discretionary of course and we could reduce or cut if we had to. We "spend" a lot on contributing to my 401k, HSA and so on but that is also discretionary. If my income dropped dramatically, we'd just not contribute or contribute less.

When I am 65 I will be on Medicare but still working so Part B might be expensive so maybe our health insurance in today's dollars would drop by $400, it will be 6 years after that before my wife gets Medicare. One month after I turn 66 the mortgage on our rental will be paid off which cuts another $1500/mo off our nut.

Go through this sort of bottom up process with your numbers. How much will you actually need? If you've been living below your means then what you need should be less than you've been making. We very fortunately are doing better than $80,000 and in just seven years, the number will start to go down in today's dollars which makes this self assessment stress free.

What can you do now to lower your number if going through this exercise causes stress or anxiety?

Back to the reality of income sources. What will your Social Security be? They want you to know. What will it be if they haircut by 20%? If you believe it will be cut then go with that number. This paper reiterates a point we've made that benefit cuts will start with Millennials, not Gen-X but even if you don't believe yours will be cut, maybe go with the reduced number anyway to be conservative.

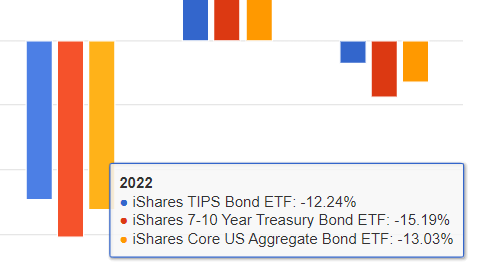

How much are you likely to end up with in your retirement accounts? If you're 60, want to retire at 66 and have $800,000, you're not likely to end up with $3 million six years from now. This example putting in $15,000 into a 60/40 fund compounding at 9% just like VBAIX did for the last 6 years would wind up with $1.4 million six years from now according to Portfoliovisualizer. That's not infallible for course but it's better than nothing. Portfoliovisualizer has a free tier for you to do this work for your numbers.

How much can you take from your portfolio? The standard default is 4%. Once you fully understand where 4% comes from, the odds that 5% is safe are very high. Every advisor has a couple of clients who withdraw way above 4-5%, I certainly do but the market of the last 15 years or so has bailed those people out. It may be problematic to expect that in the future.

What does your SS plus 4-5% of your savings add up to? Is it enough in terms of dollars and cents, what about in terms of emotional comfort? Where do you stand? Does it look like you can be resilient in case something expensive unexpectedly comes along? What something expensive that maybe is expensive like replacing a car at some point?

If you are short or otherwise not comfortable enough, what are you going to do? Will you keep working? Can you cut your expenses? Can you monetize something? Not too many people have pensions these days, do you have a source of "passive" income like from a property rental?

There's a lot of open ended questions here of course and there will be contingencies and changes that cannot be planned for, but it's just a little work to understand your numbers as you expect them to be and then be able to adapt if you do have to make changes.

Ultimately, whatever number you end up with will be your reality and you will make it work because you have to.

The information, analysis and opinions expressed herein reflect our judgment and opinions as of the date of writing and are subject to change at any time without notice. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.