Nate Geraci of the ETF Store is fond of saying "no one knows nothing" usually in the context of talking about Bitcoin but I think the sentiment also applies to the sentiment around long bonds. Here's a chart from Bespoke Investment Group.

There was a pretty wide consensus from long before the FOMC actually made that first rate cut that investors should lock into longer bonds before those rates went down and stayed down. Rates obviously did trend down and now they are trending up.

The market seems to be pricing in fewer FOMC rate cuts in the intermediate term. Will that be correct? If they follow through with rate cuts, what will that do to longer bond rates? What rates "should" do might differ from what they will do. What if they slow down on the rate cuts? What would rates do then, keeping in mind that what rates "should" do in that scenario might differ from what they will do?

The 40 year, one way trade for bonds has been over for a couple of years. For those couple of years, I have been banging the drum that bonds with duration have become a source of unreliable volatility.

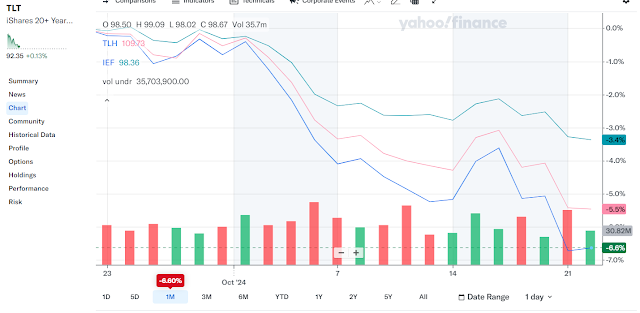

The drop in TLT over the last month is greater than one year's interest (or dividend if you own the ETF), same with TLH which tracks 10-20 year treasuries. Of course, these might come ripping back, who knows, and that is the point.

I included the following chart in yesterday's post.

Long dated treasuries are included as being a diversifier. It turns out that TLT and TLF have no correlation to the S&P 500 for now according to Portfoliovisualizer. We've made a couple of references lately to Ray Dalio using the term Holy Grail of Investing to have 15-20 uncorrelated return streams in order to get proper diversification. The above chart has nine that are low to negatively correlated to equities and the correlations amongst the nine are mostly low or negative to each other including long dated treasuries.

If it makes sense to think about long dated treasuries as just another diversifier instead some sort of core building block that many people allocate 40% to, maybe something like 4-5% is feasible? I still think long bonds are a bad hold for the reasons I've said but thinking of them as just another diversifier to have a low-mid single digit weighting casts a different light. Just because 40% is a terrible idea, there will be periods where they go up and maybe one of those periods will coincide with a large decline for equities.

The other day, I labeled global macro, certain types of long/short, risk premia and maybe even Bitcoin as You're Saying There's A Chance alts because they could go up during the next large decline, or not, there's no reliable way to know but they legitimately have a chance. Today I stumbled into a much better label from Aspect Capital via Mark Rzepczynski that in addition to global macro, certain types of long/short or risk premia and Bitcoin could include long bonds. They refer to it as unpredictability alpha. Kind of like crisis alpha, unpredictability alpha might help offset stock market volatility although calling it unpredictable alpha might make more sense.

I still think there are far better diversifiers than long bonds but if you want to play around with long bonds, it might be difficult to backtest. They went from very predictable to being very unreliable almost instantly in late 2021.

The information, analysis and opinions expressed herein reflect our judgment and opinions as of the date of writing and are subject to change at any time without notice. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

No comments:

Post a Comment